How AI and Machine Learning Are Battling Global Financial Fraud

AI, Machine Learning, and Fraud Protection

Across the global economy, fraud is a persistent problem. An estimated 26% of global citizens lost money to scams or identity theft between 2022 and 2023, culminating in financial losses estimated at $1 trillion.1 In the United States, financial institutions reported fraud losses increasing by approximately 65% between 2022 and 2023.2

While fraudsters now use artificial intelligence (AI), specifically machine learning techniques, to make old scams like phishing and identity theft swifter and more sophisticated,3 these methods are powerful tools for connecting and organizing data that may provide businesses with a significant advantage in the fight against fraud.

Fraud and the AI-enabled world

The term “artificial intelligence” was coined in the 1950s,4 but it was not until recently that AI gained the capacity and resources to solve a real-world business problem like fraud. Now, the power of more computational data, combined with a growing talent base in artificial intelligence, allows banks and financial institutions to sharpen their strategies—but it also gives bad actors new tools to perpetrate fraud.

AI, specifically machine learning and deep learning, can recognize fraudulent activities and behavior patterns within vast datasets that are beyond what the human eye can detect. Large amounts of historical data can be quickly processed and analyzed to identify new behavior patterns and spot suspicious transactions that indicate fraud.

Over time, machine learning systems may become more accurate at identifying anomalies and adapting to new types of fraud as they emerge. This helps businesses build anti-fraud systems that grow smarter and stronger at fraud prevention, identification, interception, and remediation tasks as they are continually trained on growing data sets.

The types of payment fraud machine learning can detect

Fraudsters continually seek out new ways to exploit weaknesses using technology. As they evolve and adapt their techniques, it becomes even more important for businesses to expand their fraud prevention capabilities so that any attempts at fraud are identified and dealt with quickly and comprehensively.

Some common types of payment-related fraud include:

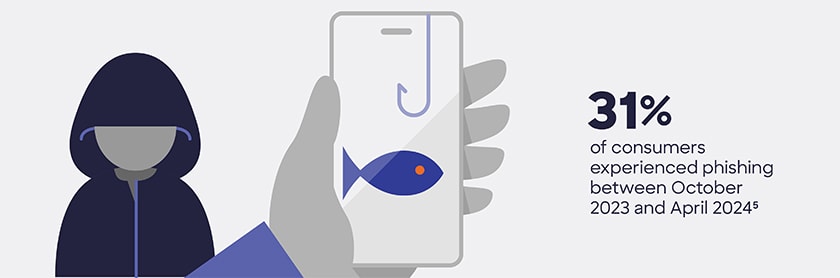

- Account takeovers, which happen when fraudsters trick a consumer or merchant into sharing usernames, passwords, and other sign-in information to access their accounts. These are frequently the result of a phishing attack.

- Card cracking, in which bots attack the payment interface of an e-commerce platform, guessing missing values for stolen card data and attempting small transactions to test whether numbers are valid.

- Chargeback fraud, in which a criminal makes a valid purchase and then disputes it with their bank or credit card company while keeping the products without paying for them, causing a chargeback to the merchant.

- Credential stuffing, in which attackers use automated bots to try to input large amounts of usernames and passwords (or partial usernames and passwords sourced from data breaches) into a login page with the goal of gaining access to some accounts.

- Fake account creation, in which automated bots create fake accounts at high speeds to give fraudsters the ability to disseminate false information, manipulate analytics, post fake product reviews, spread malware, and worse.

- Identity impersonation, which happens when criminals steal and use someone’s personal information, email, passwords, voice, and payment card numbers to impersonate them.

- Malware, which is malicious software that cybercriminals install on a merchant’s website. It gives them access to payment data and customers’ personal information.

- Man-in-the-middle attacks, in which attackers intercept unencrypted communications between a consumer’s device and a merchant’s website to access sensitive information.

How machine learning detects fraud

AI fraud detection uses machine learning algorithms to analyze behaviors and detect anomalies that indicate fraud. These systems start with a baseline of normal transaction patterns and user behaviors and then continuously monitor data to look for deviations from the norm.

As machine learning models encounter new and varied data, they fine-tune their parameters to differentiate between legitimate and suspicious activity more effectively with capabilities like:

- Anomaly detection, a deep learning technique that analyzes connectivity patterns to automatically identify unexpected changes in a dataset’s normal behavior. Anomaly detection models can help identify fraudulent activities in real-time and are frequently used to detect credit card and insurance fraud, as well as monitor for cyber threats.

- Behavioral analysis, another deep learning technique that analyzes and anticipates the behavior patterns connected to customers, merchants, devices, and accounts at a granular level across every aspect of a transaction. This data is used to build profiles that update with each new transaction, which help distinguish fraudulent behavior from legitimate behavior and inform decisioning about what transactions are approved or declined.

- Continuous learning, which refers to the ability of machine learning algorithms to use new data to sharpen their accuracy and improve effectiveness over time, making it well-suited to the ever-evolving nature of fraudsters and their tactics.

- Natural language processing (NLP), another branch of artificial intelligence, machine learning that enables computers to comprehend, generate, and manipulate human language through both written and verbal forms, such as emails, calls, and chat transcripts. NLP can be used to understand sentiment through customer service center calls or through social listening. It may also preemptively detect the reasons for a call so it can be appropriately routed or escalated.

Work with proven AI and machine learning partners

Interest in AI is high across all sectors of the global economy as it is emerging as a powerful tool for organizing, connecting, protecting, comparing, and sharing data in the fight against fraud. As businesses and financial institutions stock their anti-fraud toolkits with a variety of AI technologies, it is important to bring in the right talent. Look for partners who have proven they practice the responsible use of the technology and are committed to maintaining ethical and unbiased models as they evolve, to deliver more precise insights, help inform better decisions, conduct successful fraud investigations, and ultimately protect your customers and your bottom line.

1. (2023). The Global State of Scams 2023. Global Anti-Scam Alliance. Accessed 15 March 2024 from www.gasa.org

2. (2023, December 14). Good vs. Bad: Fraud Losses at FIs Up 65% as Both Sides Turn to AI. PYMNTS. Accessed 15 March 2024 from www.pymnts.com

3. Owen, Quinn. (2023, October 11). How AI can fuel financial scams online, according to industry experts. ABC News. Accessed 15 March 2024 from abcnews.go.com.

4. Monterey, Troy. (2022, January 30). Who Started Artificial Intelligence In Business First?. International Centre for Trade and Sustainable Development. Accessed 15 March 2024 from www.ictsd.org

5. (2024, April 11). 451 Research & Discover Global Merchants Survey. 451 Research, part of S&P Global Market Intelligence.

The information provided herein is sponsored by Discover® Global Network. It is intended for informational purposes, and is not intended as a substitute for professional advice.